« Why doesn't economics cite other fields? | Main | To live in Barcelona »

April 25, 2006

Risk tolerance

ASSESSING RISK TOLERANCE WITH A SIMPLE GAMBLE

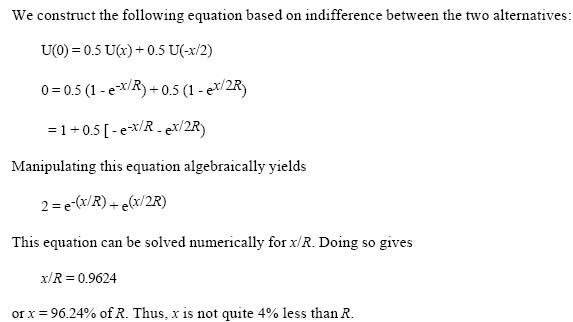

Want to estimate risk tolerance with just one question? Thanks to Bob Clemen who has written a nice piece about it in the Decision Analysis Newsletter, and to the SJDM mailing list, here's the one question:

"Suppose you face a gamble where you can win $x with probability 0.5 or lose $x/2 with probability 0.5. What is the largest x for which you would be just willing to take this gamble? I’m looking for the largest x that makes you just indifferent between taking the gamble or not."

In Clemen's book Making Hard Decisions, in the solutions manual, he gives a derivation of how to get from the respose to that question into an estimate of the risk tolerance parameter R in the exponential utility function U(x) = 1-exp(-x/R).

Another way to estimate risk tolerance is using the Distribution Builder

Posted by dggoldst at April 25, 2006 01:08 PM